The Case for Delaying OAS Payments has Improved

Canadians who collect Old Age Security (OAS) now get a 10% increase in benefits when they reach age 75. The amount of the increase isn’t huge, but it’s better than nothing. A side effect of this increase is that it makes delaying OAS benefits past age 65 a little more compelling.

The standard age for starting OAS benefits is 65, but you can delay them for up to 5 years in return for a 0.6% increase in benefits for each month you delay. So, the maximum increase is 36% if you take OAS at 70.

A strategy some retirees use when it comes to the Canada Pension Plan (CPP) and OAS is to take them as early as possible and invest the money. They hope to outperform the CPP and OAS increases they would get if they delayed starting their benefits. In a previous post I looked at how well their investments would have to perform for this strategy to win. Here I update the OAS analysis to take into account the 10% OAS increase at age 75.

This analysis is only relevant for those who have enough other income or savings to live on if they delay OAS. Others with no significant savings and insufficient other income have little choice but to take OAS at 65.

OAS payments are indexed to price inflation, and the increases before you start collecting are also indexed to price inflation. So, the returns that come from delaying OAS are “real” returns, meaning that they are above inflation. An investment that earns a 5% real return when inflation is 3% has a nominal return of (1.05)(1.03)-1=8.15%.

In many ways, the OAS rules are much simpler than they are for CPP, but two things are more complex: the OAS clawback and OAS-linked benefits. For those retirees fortunate enough to have high incomes, OAS is clawed back at the rate of 15% of income over a certain threshold. This complicates the decision of when to take OAS. Low-income retirees may be eligible for other benefits once they start collecting OAS. These factors are outside the scope of my analysis here.

A One-Month Delay Example

Suppose you’re deciding whether to take OAS at age 65 or wait one more month. For the one month delay, the OAS rules say you’d get an additional 0.6%. So, for the cost of one missed payment, you’d get 0.6% more until you reach 75. After that, you’d be getting 0.66% more.

The real return you get from delaying OAS depends on your planning age for the end of your retirement. To choose a planning age of 80, 90, or 100, people often imagine when they might die, but this is the wrong way to think about this choice. If you're going to spend carefully in case you live a long time, then your planning age should reflect this. It shouldn’t be “might I die before I get to 80.” It should be “am I so sure that I’ll die before 80 that I’m willing to spend down all my savings before I turn 80?” Viewed this way, I choose a planning age of 100.

For a planning age of 100, the real return from the one-month delay is a little over 7%. So, your investments would have to average 7% plus inflation to keep up if you chose to take OAS right away and invest the money.

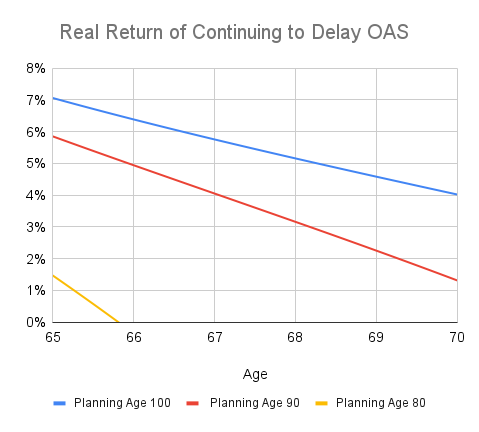

All the One-Month Delays

The following chart shows the real return of delaying OAS each month for a range of retirement planning ages, based on the assumption that the OAS clawback and delaying additional benefits don’t apply. The returns are slightly higher than they were before CPP payments rose 10% at age 75.

The case for delaying OAS isn’t nearly as compelling as it is for delaying CPP. However, those with a retirement planning age of 100 get real returns above 4% for delaying all the way to age 70. I plan to wait until I’m 70 to take OAS.

For a retirement planning age of 90, delaying OAS to 68 or 69 makes sense. However, those whose health is poor enough that they plan to age 80 or less should just take OAS at 65.

When it comes to delaying CPP or OAS, I also look at it this way. Assume I retire at 65, but my situation changes later on, such that it makes sense for me to go back to work. At age 66, that's likely a very realistic option. At age 86, it may not be. There may come a time in my life, where working - even as the proverbial greeter at Walmart - is no longer possible. I won't be getting a private pension. It will be my portfolio and government benefits. The government benefits (CPP, OAS) are materially better than any fixed income I can get in my portfolio (I'm assuming good health). To decrease risk, I want to diversify between the two. And that means delaying CPP and OAS.

ReplyDeleteAlso, the increase in return associated with delay is somewhat similar to cap gains. You don't pay tax on unrealized cap gains, and you don't pay tax on the increase in benefits due to delay, until you start taking benefits. There's a tax deferral associated with delaying.

That's a sensible point of view. Larger CPP and OAS means lower risk in the future.

DeleteI definitely hit the "Like Button" on the above post. Guaranteed is beautiful.

ReplyDeleteMy situation is more complicated. I currently have a $60,000 company pension and $25,000 annual dividends (as it currently stands) in an open account. Those dividends will grow - once I begin RRIFing my $600,000 RRSP and re-invest some of that in more stocks, and also assuming dividend increases. Fortunately I can split some pension / RRIF with my wife, but that dreaded dividend gross-up will likely still hurt me.....and then there is the delaying of my CPP until 70 where I will be getting close to the max CPP payout at that time.

I would love to delay OAS as per mentioned, but it likely is not an option for me.

For my own situation, I found it necessary to simulate outcomes for a wide range of possible drawdown strategies to settle on the best one. I don't know of any way to determine what's best for you without simulation.

DeleteOne thing my wife and I did for decades was to spend only my money and save all of hers. Now we have comparable net worths (as judged by CRA) which makes income balancing to minimize taxes much easier. You might consider trying something similar if your net worths aren't balanced and your wife has income or inheritances or other money coming in that is in her name.

Another minor hack I suggest to people is that if they would be receiving first OAS payment in December (or maybe even in November), then it will likely be taxed at a higher marginal tax rate. Since many retirees will be in a lower tax bracket once retired, there is a case for delaying the start of OAS until the start of the year.

ReplyDeleteHi Bob, That's a good suggestion for those who start OAS soon after retiring.

DeleteOne can make a similar argument for timing of CPP. And I've heard of tax planning being used to time retirement. For example, instead of retiring Dec 31, wait another month. For some, the aftertax monthly income from that extra January will be higher than any other aftertax monthly income in their life.

DeleteThat's true. Although I'd really like people to consider waiting much longer than just one extra month to see if it makes sense for them.

Delete